The market for business neobanks has matured into two distinct segments: platforms optimized for rapid-growth tech startups and those built for independent small businesses. Novo and Mercury represent the leaders of these respective categories.

While both platforms offer no-fee checking accounts and operate via partner banks, their feature sets are optimized for different operational workflows. Choosing between them depends largely on whether a business prioritizes integrated bookkeeping tools or advanced treasury and API capabilities.

Symmetric comparison table

| Feature | Novo | Mercury |

|---|---|---|

| Primary Audience | Freelancers, SMBs, E-commerce | Startups, Venture-backed Biz |

| Monthly Fee | $0 | $0 (Standard) |

| Cash Deposits | No (via Money Order) | No |

| ATM Access | Global Reimbursement | Allpoint Network (No Fee) |

| Outgoing Wires | International Fee Applies | No Domestic or International Fee |

| Integrations | Stripe, Shopify, QuickBooks | Specialized Startup API, Zapier |

| Yield Account | No | Yes (Mercury Treasury) |

How each product is structured

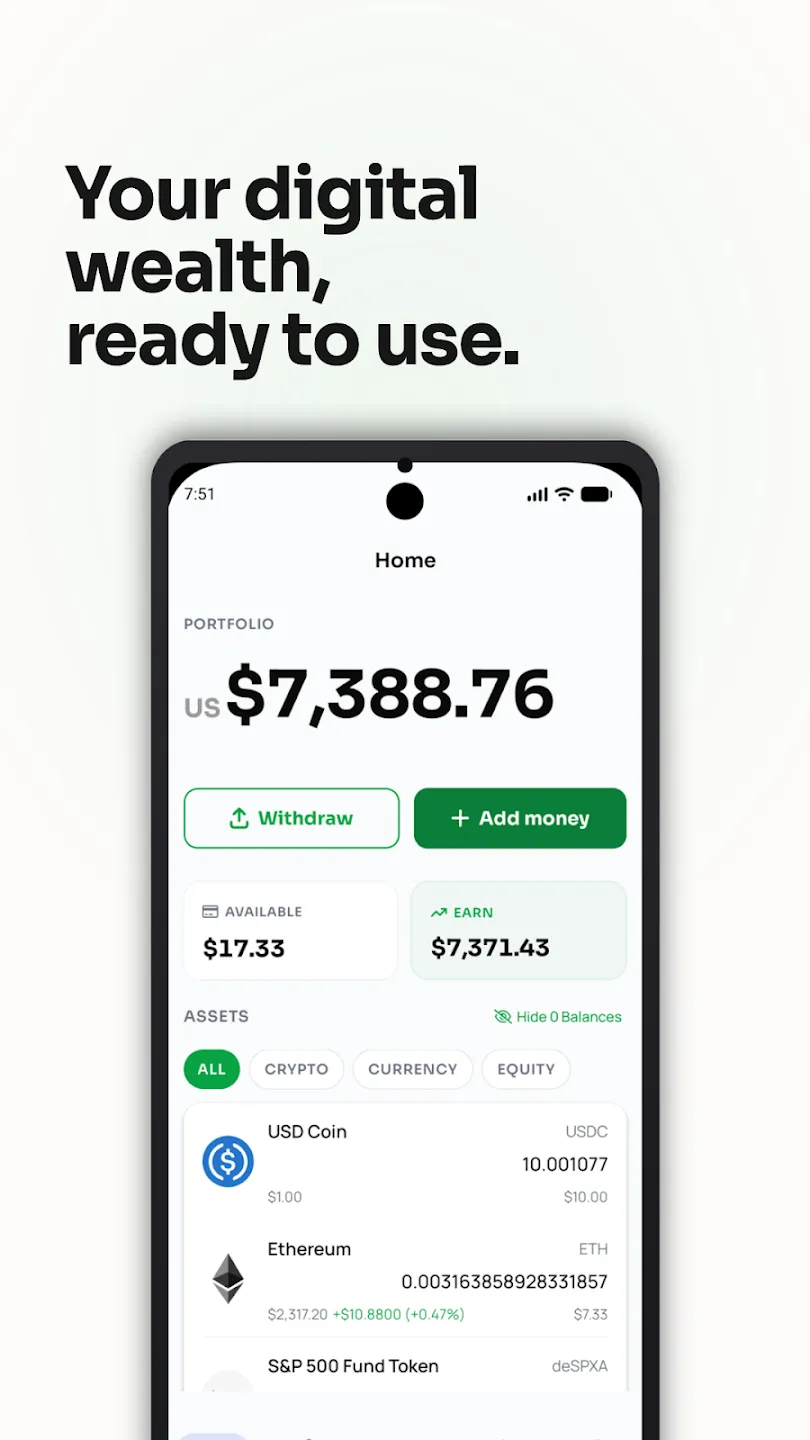

Novo is structured as a software layer on top of Middlesex Federal Savings, F.A. It emphasizes a mobile-first experience designed for individual owners who manage their own finances. The platform architecture revolves around “Novo Reserves,” allowing users to tag funds for specific liabilities like taxes directly within a single account.

Mercury operates as a fintech platform with banking services provided by Choice Financial Group and Column N.A. Its structure is more complex, designed to handle larger capital balances and multiple team members. Mercury utilizes a sweep network to provide up to $5 million in FDIC insurance, whereas Novo typically relies on the standard $250,000 per-depositor limit.

Fees and pricing mechanics

Both platforms eliminate many of the “hidden” costs associated with traditional banking, such as monthly maintenance and overdraft fees. However, their approaches to transaction costs differ.

- Novo Fees: Novo focuses on eliminating the cost of cash access. While it does not own ATMs, it reimburses all ATM fees globally. Outgoing international wires carry a fee, typically managed through a third-party partner like Wise.

- Mercury Fees: Mercury focuses on eliminating the cost of moving money. It offers unlimited no-fee domestic and international wires in USD. For ATM access, it utilizes the Allpoint network for fee-free withdrawals but does not typically reimburse out-of-network fees.

Limits, eligibility, and availability

Both platforms require a U.S.-based business entity (LLC, Corporation, or Sole Proprietorship) and a valid EIN.

Novo is generally more accessible for very small businesses and sole proprietors. Its application process is streamlined for individuals and focuses on compatibility with retail platforms like Shopify and Amazon.

Mercury is optimized for companies with larger teams and more complex funding structures. It is the default choice for venture-backed startups due to its compatibility with incorporation services like Stripe Atlas. Mercury also has higher transaction limits for ACH and wires, which can be custom-negotiated for high-growth companies.

Tradeoffs and constraints

The choice between Novo and Mercury involves selecting one set of trade-offs over another.

- The Novo Tradeoff: Users gain superior bookkeeping integrations and ATM flexibility but lose the ability to earn yield on idle cash. Novo’s features are “baked-in” to the app, making it easier for a single user to manage but less flexible for a developer who wants to build custom financial workflows.

- The Mercury Tradeoff: Users gain access to professional treasury tools and a robust API for an “automated” back office but lose the ability to deposit money orders easily or get ATM reimbursements. Mercury’s interface is built for the web first, which may feel overpowered for a simple solo operation.

Neither platform currently supports physical cash deposits or provides traditional branch services like notary or cashier’s checks.

See also: Novo Review, Mercury Review, Relay vs Mercury