NALA is a digital remittance platform that specializes in sending money from the United Kingdom, the United States, and the European Union to African markets. The system is designed to bridge the gap between traditional international banking networks and the mobile money infrastructure that dominates many African economies.

This review documents the structural mechanics, cost transparency, and operational trade-offs of the NALA platform.

What NALA is structurally

NALA is a mobile-first money transmitter that operates as a licensed financial service provider in its sending markets. It does not function as a traditional bank but rather as a payment relay system that utilizes local liquidity pools to facilitate cross-border transfers.

The platform is built on a “local payout” model. Instead of sending money through the SWIFT network, which often involves multiple intermediary banks and delays, NALA maintains reserves in both the sending and receiving countries. When a user initiates a transfer in the UK, NALA receives the funds in British Pounds and simultaneously instructs its local African partners to release the equivalent amount in local currency.

This structure allows the system to bypass the high fees and slow settlement times typically associated with correspondent banking. NALA focuses its infrastructure primarily on corridors into countries such as Kenya, Tanzania, Ghana, Rwanda, and Uganda, where it integrates directly with local bank rails and mobile money operators.

How the system works in practice

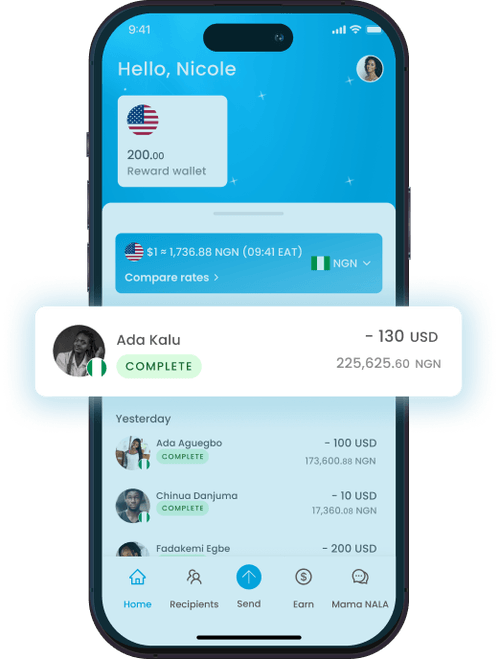

The NALA user experience is restricted entirely to its mobile application, with no browser-based interface available for personal transfers. After downloading the app, users must undergo a Know Your Customer (KYC) verification process, which typically requires a government-issued ID and proof of address.

Once verified, the user connects a funding source, such as a bank account or a debit card. The transfer process follows a straightforward sequence: the user selects the destination country, enters the amount, and chooses a payout method. The system provides a real-time quote showing the exchange rate and the exact amount the recipient will receive before the transaction is finalized.

Payouts are generally delivered via two primary channels:

- Bank Deposits: Funds are sent directly to a recipient’s traditional bank account in the destination country.

- Mobile Money (MoMo): Funds are sent to digital wallets managed by telecommunications companies, such as M-Pesa in Kenya or MTN MoMo in Ghana.

The platform also includes secondary features like “Bill Pay,” which allows users to pay utility bills directly in African countries, and “Buy Goods,” which facilitates payments to local merchants. These features represent a shift from simple person-to-person remittance toward a more integrated cross-border payment utility.

Fees and pricing mechanics

NALA markets its service as having “no hidden fees,” a claim that refers to the absence of traditional flat-rate transaction fees for most major corridors. However, like most remittance providers, the system is not free; it generates revenue through an exchange rate markup.

The exchange rate markup is the difference between the mid-market rate (the “real” rate banks use to trade with each other) and the rate NALA offers to its users. Typically, this markup ranges between 0.5% and 2.0%, depending on the specific currency pair and market volatility. While NALA often provides more competitive rates than legacy banks or traditional retail agents like Western Union, its total cost may be higher than providers that use the mid-market rate but charge a transparent service fee.

For very low-value transfers, such as those under €10 or £10, NALA has historically implemented a small transfer policy. In these cases, users may be allowed a specific number of free small transfers per month, after which a nominal fee (often around €0.50) is applied to cover the fixed costs of processing the transaction.

Limits, eligibility, and availability

The NALA system enforces transaction limits that are determined by the user’s verification level and the regulations of both the sending and receiving countries. New users typically start with lower daily and monthly limits, which can be increased by providing additional documentation, such as proof of income or a bank statement.

Limits are categorized into three tiers:

- Daily Limits: The maximum amount a user can send within a 24-hour window.

- Monthly Limits: The aggregate amount allowed over a rolling 30-day period.

- Annual Limits: The total volume permitted per calendar year.

Eligibility is restricted to residents of the UK, US, and certain EU countries. Recipients must be located in one of NALA’s supported African corridors. Furthermore, the recipient’s payout method may have its own constraints; for example, mobile money wallets often have a maximum balance limit (e.g., KES 500,000 for M-Pesa), which can cause a NALA transfer to fail if the recipient’s wallet is already near its capacity.

Trade-offs, risks, and limitations

The primary trade-off of using NALA is the balance between convenience and absolute cost. While the app offers a highly streamlined experience and specialized features for African corridors, it is not always the cheapest option for every transfer.

Pros and Efficiency:

- Speed: By using local liquidity, transfers to mobile money wallets are often delivered in seconds.

- Specialized Features: The ability to pay bills and buy goods directly in Africa is a significant differentiator for the diaspora community.

- User Interface: The app is designed for modern mobile users, with features like “Repeat Transfer” and real-time tracking.

Risks and Constraints:

- App-Only Access: Users who prefer to manage their finances on a desktop or through a web browser are unable to use NALA.

- Corridor Specificity: NALA is highly optimized for Africa but does not offer the global reach of platforms like Wise or Revolut.

- Exchange Rate Volatility: Because NALA uses a markup model, the effective cost of a transfer can fluctuate throughout the day as the mid-market rate moves, even if the “fee” remains at zero.

As with any digital financial service, there is a risk of transaction delays due to regulatory checks or technical issues with local payout partners. Users are advised to verify the recipient’s details carefully, as international money transfers are generally irreversible once the funds have been settled into the recipient’s account or wallet.

See also: Best Money Transfer for Africa, How International Transfers Work, Remittance Fees Explained