Paysend operates as a digital-first payment platform specializing in international money transfers and multi-currency banking services. The system is designed to facilitate movement between cards and bank accounts across different jurisdictions.

The platform utilizes a proprietary card-to-card technology developed in partnership with major global payment networks. This infrastructure aims to simplify the cross-border remittance process for individual and business users.

How does card-to-card technology bypass intermediary banks?

Traditional international transfers often require navigating complex intermediary banking networks and entering detailed routing information. Paysend addresses this by utilizing the existing infrastructure of global card networks like Visa and Mastercard.

This mechanism allows funds to move directly between the card numbers of the sender and the recipient. When a sender initiates a transfer, the platform draws funds from their linked debit or credit card.

Instead of routing through the SWIFT network, the platform sends instructions through the card network to push the balance to the recipient’s card. Because it utilizes card networks, these transfers often settle within minutes, differing from traditional bank wires.

This model allows users to send money even if the recipient does not have a traditional bank account, provided they possess a supported card. The bypass of traditional banking rails reduces the technical steps required for cross-border settlement.

Why does Paysend utilize fixed fees and exchange rate spreads?

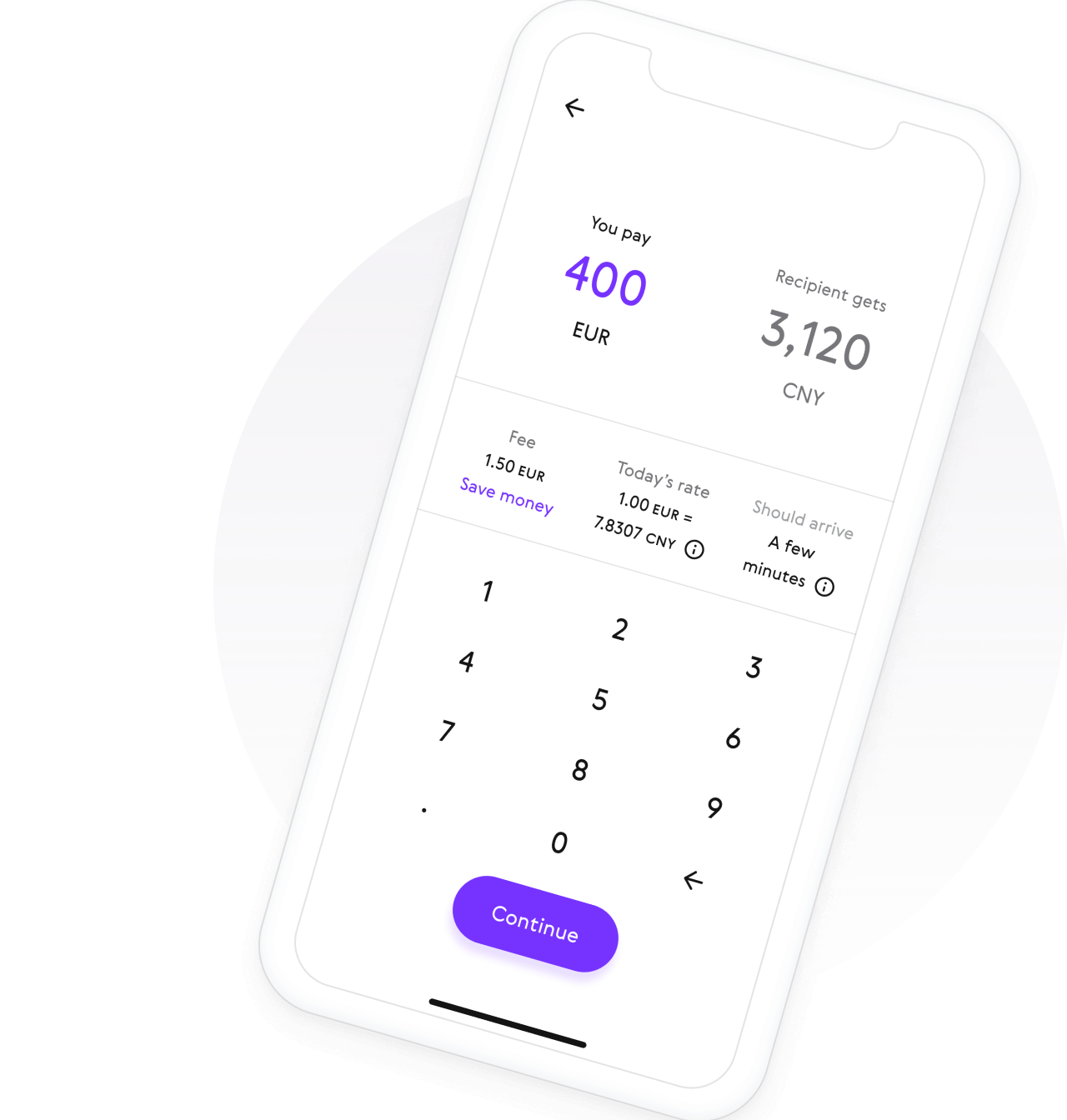

The platform utilizes a pricing model characterized by fixed transaction fees and embedded exchange rate markups. For many international corridors, the platform charges a flat, fixed fee regardless of the total amount sent.

This fee is typically set at $2 from the United States, £1 from the United Kingdom, or €1.50 from the Eurozone. Because the fee remains constant, the effective cost percentage decreases as the transfer size increases.

In addition to the fixed fee, the platform generates revenue through an exchange rate markup. This is a spread added to the mid-market rate found on global currency markets.

The specific rate is displayed in the mobile app or website before the user confirms the transaction. Knowing the exact rate upfront allows the sender to calculate the final amount received without hidden deductions.

How does Paysend Link manage recipient information?

Managing recipient information across different countries can be a barrier to regular remittances. The platform addresses this through a feature called “Paysend Link” which uses mobile phone numbers as identifiers.

This system allows a sender to initiate a transfer using only the recipient’s mobile phone number. The platform then sends a secure link to the recipient via SMS or a messaging application.

The recipient clicks the link and enters their own card or account details to claim the funds. This shifts the responsibility for providing accurate banking information from the sender to the receiver.

Senders do not need to store the recipient’s sensitive financial details on their own device. The mechanism ensures that data is provided directly to the secure platform by the party controlling the account.

How do regulatory frameworks safeguard Paysend customer funds?

As a global financial institution, the platform operates under various regulatory frameworks to ensure the legality and safety of funds. In the United Kingdom, the platform is authorized and regulated by the Financial Conduct Authority (FCA).

In the United States, it operates through partnerships with regulated banks and holds state-level money transmitter licenses. Under its EMI status, the platform is legally required to “safeguard” customer funds in dedicated bank accounts.

These accounts are separate from the company’s operational funds, ensuring they remain available even during financial distress. Unlike traditional bank deposits, these safeguarded funds are not typically covered by government-backed deposit insurance schemes.

The protection comes from the legal separation of assets rather than a central insurance fund. This regulatory structure is standard for electronic money institutions operating in the UK.

What are the practical limitations of the service?

Several factors influence the practical application of the platform for different types of transfers. While the platform supports over 170 countries, not every country allows both sending and receiving funds.

Every user must undergo Know Your Customer (KYC) verification, requiring government-issued identification. The system imposes daily and monthly limits on the volume of money that can be moved.

These limits are tiered and can only be increased by providing additional verification to the compliance department. Network availability and regional regulations can also influence the speed and success of specific transfer corridors.

Understanding these technical and geographic boundaries is necessary for assessing the system’s utility for specific routes. The platform remains a specialized remittance tool rather than a full-service banking alternative.

Common questions

How long does a card-to-card transfer take?

Most transfers settle within minutes because they utilize the near-instant authorization systems of global card networks. However, some receiving banks may take longer to credit the funds to the user’s available balance.

Is Paysend a bank?

No, Paysend is an Electronic Money Institution (EMI) and a money transmitter. It does not provide traditional banking features such as overdrafts, lending, or government-insured savings accounts.

Can I send money without a card?

While the platform specializes in card-to-card transfers, it also supports account-to-account transfers in certain corridors. The availability of bank-led funding and payout depends on the specific country pairs involved.

What are the common misconceptions about Paysend?

“Fixed fees always make it the cheapest option.” The total cost includes both the fixed fee and the exchange rate markup. For smaller transfers, a percentage-based markup on a lower rate from a competitor might result in a lower total cost.

“Card transfers are identical to bank transfers.” The underlying networks are different; card-to-card transfers rely on payment processors like Visa Direct. This distinction affects how funds are routed and the types of data required for authorization.

“Safeguarded funds are protected by the FDIC.” In the US, funds may be held in partner bank accounts, but the platform itself is not an FDIC-insured bank. Protection mechanisms for EMIs center on the strict legal separation of customer and company assets.